The Financing Process

Understanding the Home Loan Process

From pre-approval to closing, the right guidance makes a difference.

For many buyers, financing is one of the most important parts of the home buying process. Working with a trusted lender can help you understand your budget, loan options, monthly payment range, and what to expect before closing. At Jay Day And The Day Home Team at LPT Realty, we encourage buyers in Frederick, MD and surrounding areas to speak with a qualified mortgage professional early so they can move forward with confidence.

Getting pre-approved is often one of the first steps because it helps define your buying power and shows sellers that you are financially prepared. As you move through the process, your lender will help guide you from application to underwriting to closing. Reviewing the basic steps ahead of time can make the process feel much easier to understand.

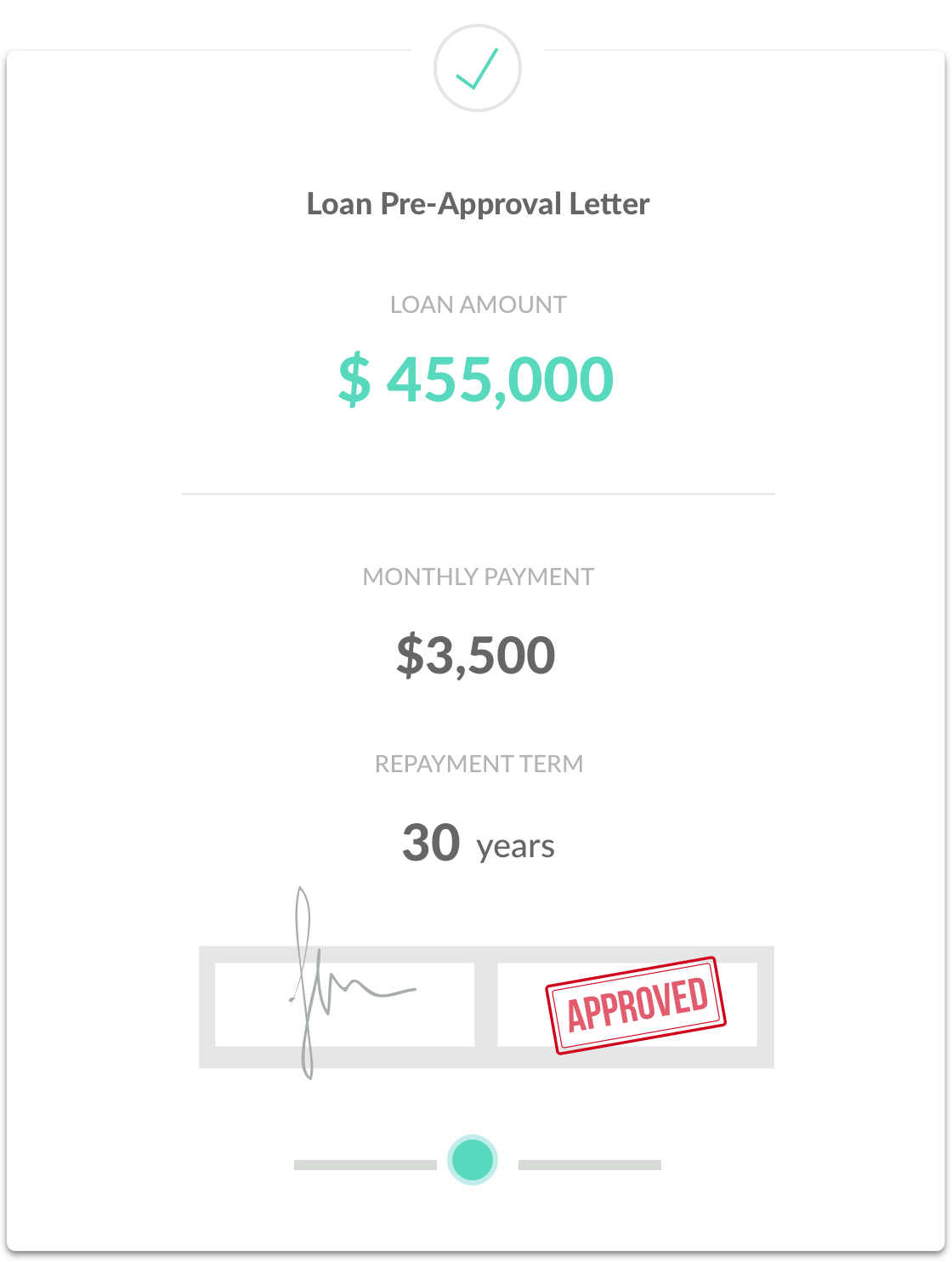

Step One:

Get Pre-Approved for a Home Loan

Before you start shopping for homes in Frederick, MD, one of the smartest first steps is getting pre-approved for a mortgage. Pre-approval helps you understand your budget, gives you a clearer picture of your buying power, and shows sellers that you are ready to make a serious offer.

To get pre-approved, your lender will review your income, assets, debts, and credit profile to determine how much you may be able to borrow. This process often includes documents such as pay stubs, W-2s, tax returns, bank statements, and a credit check.

There are several loan programs available, and the right option depends on your financial situation, goals, and preferences. A trusted lender can explain your options and help you choose a loan program that fits your needs.

What documents do you need for pre-approval?

Most lenders will ask for items like recent pay stubs, W-2s, tax returns, bank statements, and a credit check.

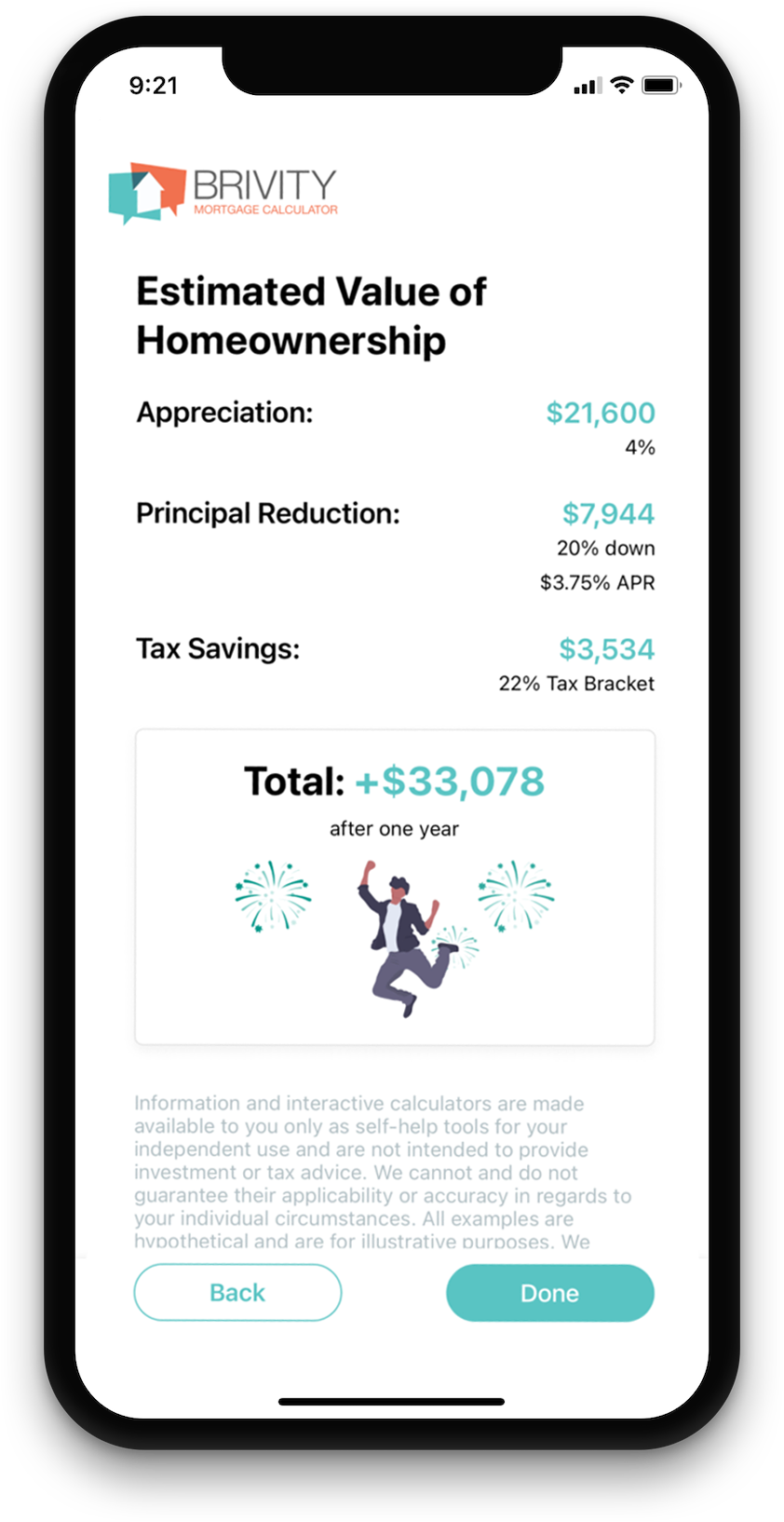

ESTIMATE YOUR MONTHLY PAYMENT

Get a clearer picture of what a home may cost each month before you buy

Estimating your monthly mortgage payment can help you better understand your budget as you search for a home in Frederick, MD and surrounding areas. This calculator gives buyers a simple way to estimate costs that may be included in a monthly payment, such as principal and interest, property taxes, homeowners insurance, HOA dues, and private mortgage insurance.

Keep in mind: Your actual monthly payment may vary based on loan terms, interest rate, taxes, insurance, and lender requirements.

Price

Annual Tax

Loan Term (Years)

Down Payment %

Interest Rate %

Monthly HOA

Monthly Insurance

$3,198.20

Estimated Monthly Payment

Principal

$2,398.20

(75.0%)Taxes

$500.00

(15.6%)HOA

$100.00

(3.1%)Insurance

$200.00

(6.3%)Step Two:

Find the Right Home Loan

Once you are pre-approved, the next step is choosing a loan option that fits your goals, budget, and comfort level. Working with a trusted local lender can help you compare rates, loan programs, down payment options, and monthly payment scenarios so you can make a more informed decision.

At Jay Day And The Day Home Team at LPT Realty, we help buyers in Frederick, MD and surrounding areas connect with lending professionals who can explain the options clearly and help you move forward with confidence.

Step Three:

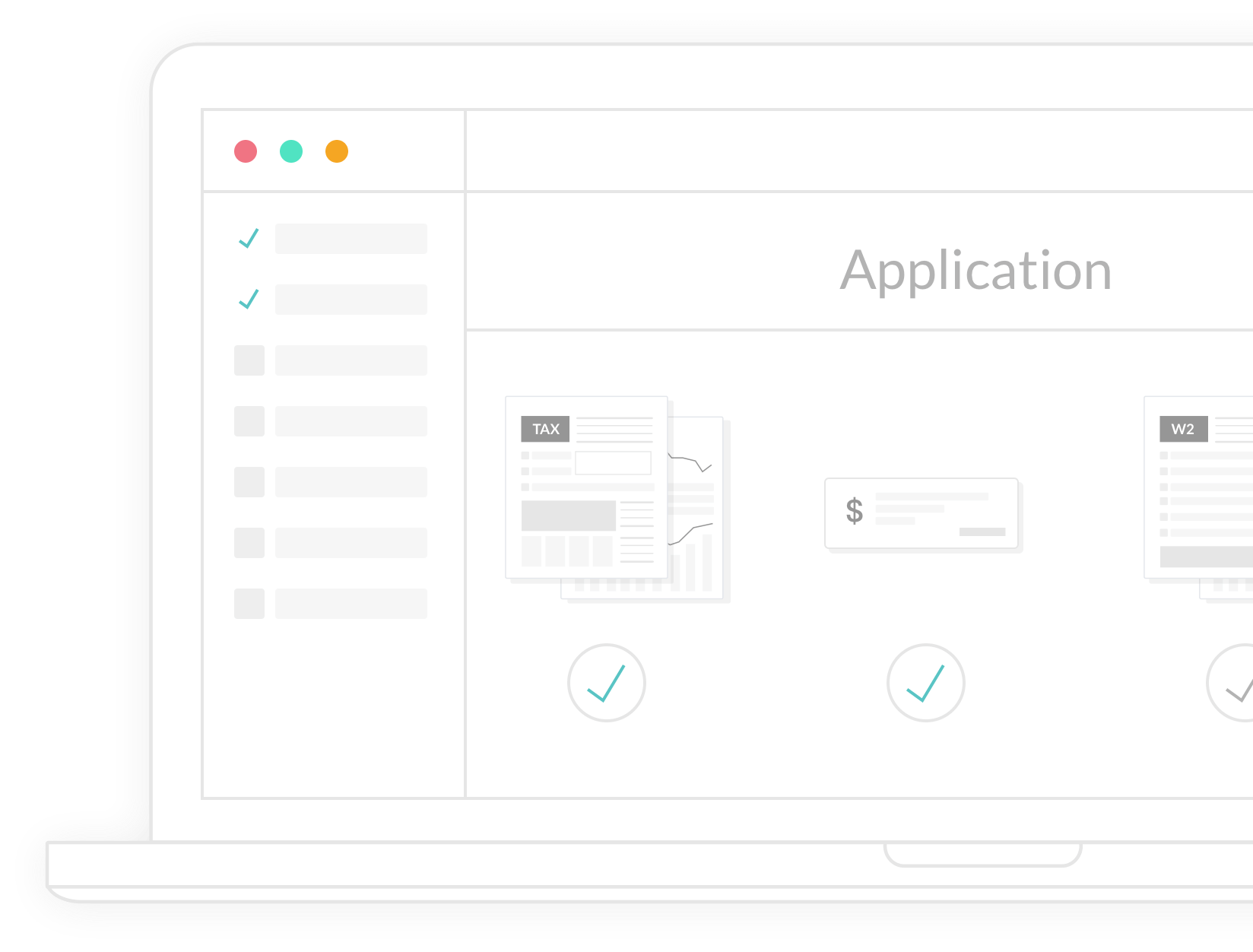

Loan Application and Processing

Once you find the right home and your offer is accepted, the next step is completing your full mortgage application. Your lender will help you finalize the application, review down payment details, and explain any loan-related costs and fees.

After that, your file moves into processing, where your financial documents are reviewed and verified. During this stage, your lender will also order the home appraisal and title work as part of the transaction.

The loan file is then submitted to underwriting, where it is reviewed to make sure everything meets lending guidelines. It is common for buyers to be asked for additional documents or clarification during this stage, so do not be surprised if a few follow-up items come up along the way.

Is it normal for the lender to ask for more documents?

Yes. During processing and underwriting, it is common for lenders to request updated paperwork or clarification before final approval.

Step Four:

Closing on Your New Home

Once your loan is approved, the final steps usually include setting up homeowners insurance, reviewing your closing information, and getting ready to sign the final paperwork. Your documents are sent to the title company, and the closing is scheduled so you can complete the purchase of your new home.

At closing, you will sign the required documents and pay any remaining funds needed to complete the transaction. After the paperwork is finalized and the deed is recorded, the home is officially yours.

When do you officially own the home?

You officially own the home after the closing documents are signed and the deed is recorded.